CDs are the most secure way to grow your money and take control of your financial life.

A certificate of deposit is a financial product offered by banks and credit unions to help investors save their money while earning a decent return on their investment. For an extensive explanation on CDs, check out what certificate of deposits are and how they work.

A key aspect of opening a CD is shopping around for the best rates in the market because institutions offer different CD menu rates.

A certificate of deposit is a low-risk investment that comes with several benefits to investors.

1. Easy to open

With proper documentation, opening a CD is very simple. Most banks will require you to visit their branch in person to open a CD, while others have online applications, which makes the process even more straightforward and can take between 10 to 20 minutes. You can then transfer your funds from your checking or savings account into a CD.

» Explore your options, take a look at the best certificate of deposits

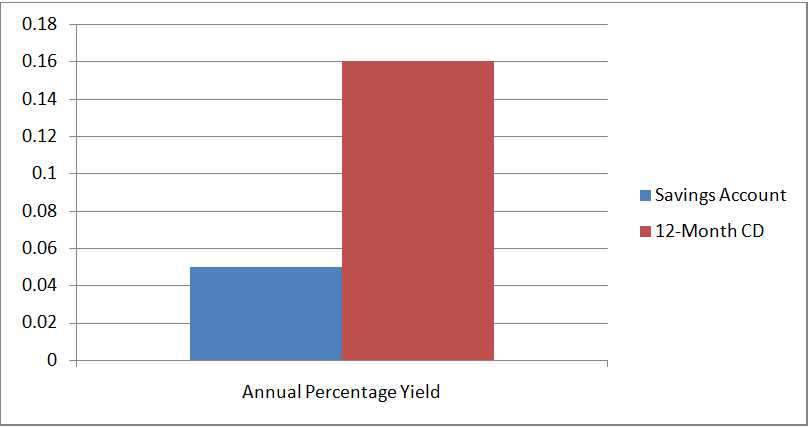

2. Better interest rates

Certificates of deposit offer the best interest rates in the market compared to savings accounts or money markets.

For instance, the national rates for CDs range from a 0.16% annual percentage yield (APY) for a 12-month CD to 0.34% for a 60-month CD, while the savings account has a 0.05% APY, as shown below. Therefore, investors earn more for saving their money in a CD for one year than in traditional savings accounts for the same period.

While shopping around to find the best rate for your CD, you may find an institution offering a way better rate if you have large deposits or if you are willing to take longer-term CDs. An online bank may also have better CD rates than your traditional brick-and-mortar bank.

3. Fixed rates

Financial markets experience a lot of fluctuations, especially the bond, stock and real estate markets, making returns from an investment very unpredictable.

A fixed certificate of deposit term works differently from these markets, locking your funds in a fixed interest rate for the CD term you have chosen. The locked interest rate will not be influenced by market changes until its maturity.

The following are two different interest rates to consider when weighing the benefits of having a certificate of deposit:

- A fixed-rate CD – pays out a uniform interest rate throughout the CD term. A 5-year CD with 2.0% APY, for instance, earns interest at a constant rate regardless of a rise or fall in the interest rate during the CD period.

- Adjustable-rate CD – the institution will set the interest rate when you are opening a CD but will give you an option to adjust the rate during the period. You will, however, have a limited number of times to adjust the rate.

4. Predictable returns

CDs have fixed rates and low risks enabling investors to forecast their returns accurately.

The interest rate is compounded when calculating the final payment. The APY is fixed over the CD term; hence the bank cannot change your earnings during the period allowing you to predict the final amount you will receive correctly.

Knowing exactly when and how much you will receive from an investment helps you plan ahead without any risk that your money will fluctuate.

5. Protected funds

Your funds are protected in two ways; the first is that the fixed rates guarantee fixed returns after maturity. The locked rate cannot be changed during the CD term meaning the returns cannot reduce or increase.

The second way CDs protect your funds is the insurance by the Federal Deposit Insurance Corporation (FDIC) for banks and National Credit Union Administration (NCUA) for credit unions. Your deposit in a CD is protected up to $250,000 in an FDIC or NCUA insured institution. Some institutions also have private insurance to protect against bankruptcy.

To take advantage of this benefit, choose an institution that offers insurance and not deposit more than the limits provided. You can spread your funds among several institutions if you have more than $250,000. This way you can maximize your insurance coverage.

6. Shoppable rates

You are not limited to one institution when opening a CD and definitely not one CD; you can have several CDs with different institutions.

Financial institutions set terms and rates for their CD menu, which are different to encourage investors to save with them. Shopping around when opening a CD improves your chances of having the best rates and returns on your deposit. Generally, online banks have better rates because of their low costs and expenses.

7. A wide selection of terms

Are you saving for a vacation in a few months or for your child’s college fund? One of the key benefits of having a certificate of deposit is that you can safely put aside your money for any period to meet your financial goals.

With a wide selection of terms, a CD can run from weeks to several months, with more extended periods having the highest rates.

You can also have a CD term that matures right before you require a withdrawal such as a 60-month CD. This CD has the highest APY and would be suitable for your a long-term investment such as your child’s educational fund.

8. CDs have low or no fees

CDs have little or no fees on deposits as most banks do not charge monthly fees. Investors, therefore, do not have to worry about banks deducting fees from their CD earnings.

One fee you could incur with your deposit is the early withdrawal penalty, which may be imposed by your institution should you take your money before maturity. Any penalties, costs, and fees are subject to the agreement when signing up. So before signing for a CD, carefully read the disclosure statement on fees and penalties applied by the institution.

Some banks also offer no-penalty CDs that do not impose penalties on early withdrawals and may be a better option if you anticipate an emergency during the CD period.

How to benefit from your CD

Certificates of deposits serve both short-term and long-term financial goals. Timing is essential when planning for your financial goals with a CD.

One challenge you face with a certificate of deposit is liquidity, where you may not access your funds until maturity. If you do not time your CD to align with your projected purpose properly, the funds may not fulfill their purpose, and accessing the money before maturity may be penalized.

A CD ladder can be of assistance to mitigate liquidity challenges. Instead of having one 5-year CD with all your money, you can divide your total amount into smaller amounts and invest in several CDs with different maturity dates.

As the different CDs mature, reinvest them into top-rate 5-year CDs, and you will end up with a portfolio of 5-year CDs, all with high APYs. The CDs will be maturing every 12 months, improving the accessibility of your funds.

Final thoughts

There are several benefits to a certificate of deposit and they provide invaluable peace of mind regarding your investment.

Even though other financial products may provide higher returns, there is uncertainty involved. Hence, CDs are the preferred option because of their steady, low-risk, and reliable growth. They are an excellent choice for investors who want to earn a decent interest in an FDIC or NCUA insured account over a fixed period.

We want to hear from you, and we encourage lively discussions among users. Leave a comment below on this topic.